Summer Destructive Insured Losses: A Comprehensive Analysis of Weather Impacts

The summer months, traditionally associated with leisure and outdoor activities, are increasingly recognized as a period of significant risk for destructive insured losses driven by severe weather events. These losses, encompassing damage to residential, commercial, and infrastructural properties, impose substantial financial burdens on individuals, businesses, and the insurance industry. Understanding the multifaceted nature of summer weather hazards and their impact on insured assets is crucial for risk mitigation, effective claims management, and sustainable insurance market stability. This analysis delves into the primary meteorological phenomena that contribute to these losses, examines their evolving trends, quantifies their financial consequences, and explores strategies for adaptation and resilience.

Thunderstorms, a hallmark of summer weather, are a potent source of destructive insured losses. These convective storms are characterized by lightning, heavy rainfall, strong winds, and hail. Lightning strikes, while often associated with fires, can also cause direct electrical damage to electronic equipment, surge protectors, and even structural components of buildings. The sheer intensity of heat and humidity during summer months often fuels the development of supercell thunderstorms, which are capable of producing some of the most violent weather on Earth. These storms are the primary drivers of tornado outbreaks and derecho events, both of which can cause widespread and catastrophic damage. Residential properties are particularly vulnerable to wind damage from these storms, with roofs being torn off, siding being ripped away, and windows being shattered. Commercial properties, with their larger footprints and often more exposed infrastructure, also suffer significant damage, impacting business operations and supply chains. The economic fallout extends beyond immediate repair costs, encompassing business interruption, loss of inventory, and temporary relocation expenses. For the insurance industry, managing the volatility and increasing severity of thunderstorm-related claims presents a significant underwriting and reserving challenge.

Heavy rainfall associated with thunderstorms, and more broadly, with slow-moving or stalled weather systems, leads to significant insured losses through flooding. While coastal storm surge is a primary concern during hurricane season, inland flooding during summer months is a growing threat. This inland flooding can stem from flash floods, where intense rainfall overwhelms drainage systems and riverbanks in a short period, or from more prolonged rainfall events that lead to widespread riverine flooding. The insurable impact of flood damage is complex, as standard homeowners and commercial property policies typically exclude flood coverage, necessitating separate flood insurance policies, often obtained through government programs. The financial toll of even moderate inland flooding can be substantial, with water damage leading to structural compromise, mold growth, and the destruction of personal and commercial property. The increasing frequency and intensity of extreme precipitation events, often exacerbated by climate change, are amplifying the flood risk, leading to higher claims payouts and putting pressure on the availability and affordability of flood insurance.

Hurricanes and tropical storms, while traditionally considered a late summer and fall phenomenon, can emerge and make landfall during the summer months, delivering immense destructive power and a significant portion of annual insured losses. The primary drivers of hurricane-related damage are high winds, storm surge, and inland flooding from heavy rainfall. The sheer force of hurricane-force winds can obliterate entire communities, causing widespread structural failure, uprooting trees, and propelling debris as dangerous projectiles. Storm surge, the abnormal rise of sea levels driven by a storm’s winds, is often the most destructive element, inundating coastal areas with saltwater, leading to extensive property damage and loss of life. The inland flooding associated with the heavy rainfall accompanying these storms can persist for days, saturating the ground and exacerbating damage. The insured losses from a single major hurricane can run into tens of billions of dollars, impacting property, auto, and business interruption insurance lines. The increasing intensity of hurricanes, predicted by climate science, poses a grave threat to coastal communities and the financial stability of the insurance sector. Reinsurance markets play a critical role in absorbing the catastrophic losses from these events, but the increasing frequency and severity of hurricanes are straining their capacity.

Droughts, while not directly causing structural damage in the same way as storms, contribute indirectly to destructive insured losses and pose significant economic challenges. Prolonged periods of low rainfall lead to arid conditions that increase the risk of wildfires. Summer heat amplifies this risk, drying out vegetation and making it more combustible. Wildfires, once ignited, can spread rapidly and with devastating intensity, consuming homes, businesses, and natural resources. The insured losses from wildfires include the cost of property destruction, containment efforts by fire services, and the long-term economic impact on affected communities. Furthermore, drought conditions can impact agricultural insurance, leading to crop failures and livestock losses. The interconnectedness of these weather phenomena means that a severe drought can be a precursor to significant wildfire-related insured losses during the summer months. Climate change projections suggest an increase in both the frequency and severity of droughts in many regions, thereby escalating the wildfire risk and its associated insured losses.

The economic impact of summer destructive insured losses is multifaceted and far-reaching. For individuals, these losses can lead to financial ruin, displacement, and long-term recovery challenges. The out-of-pocket expenses for deductibles, uninsured damages, and rebuilding efforts can be overwhelming. For businesses, severe weather events can disrupt operations, lead to inventory loss, and result in significant business interruption claims. The cumulative effect of these losses can impact local economies, leading to job losses and reduced economic activity. The insurance industry bears a significant portion of the financial burden through claims payouts. High volumes of catastrophic claims can strain the financial reserves of insurance companies, potentially leading to premium increases, reduced coverage availability, or even the withdrawal of insurers from high-risk markets. This can create an affordability and availability crisis for insurance in vulnerable regions. Reinsurance plays a vital role in transferring risk from primary insurers to global capital markets, but the increasing frequency and severity of natural catastrophes are putting upward pressure on reinsurance rates.

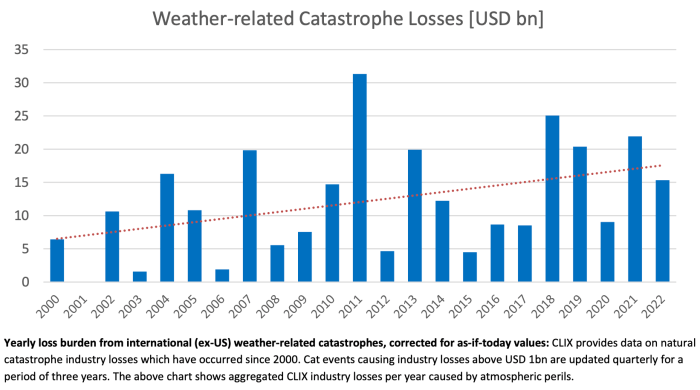

The trends in summer destructive insured losses indicate an upward trajectory, largely attributed to climate change and increased development in vulnerable areas. Climate science suggests that global warming is leading to more frequent and intense extreme weather events, including heatwaves, heavy precipitation, and stronger tropical cyclones. Warmer ocean temperatures provide more energy for hurricanes, potentially leading to more Category 4 and 5 storms. Changes in atmospheric circulation patterns can also lead to more persistent weather systems, contributing to prolonged droughts and extreme rainfall events. Simultaneously, increasing urbanization and development in coastal zones, floodplains, and wildland-urban interfaces place more insurable assets directly in the path of these hazards. This confluence of factors creates a growing risk profile for the insurance industry and for insured individuals and businesses. The economic consequences of these escalating losses necessitate a proactive approach to risk management and adaptation.

Strategies for mitigating destructive insured losses and enhancing resilience are paramount. On an individual and business level, this includes implementing robust property protection measures. For wind-prone areas, this might involve reinforcing roofs, installing impact-resistant windows and doors, and securing outdoor structures. For flood-prone areas, elevating critical infrastructure, installing backflow valves, and using flood-resistant building materials are essential. Maintaining adequate insurance coverage, understanding policy limitations, and considering separate flood or earthquake insurance are also crucial steps. For the insurance industry, data analytics and sophisticated modeling are becoming increasingly important for accurately assessing risk, pricing policies, and developing innovative insurance products that incentivize risk reduction. Investing in catastrophe modeling and early warning systems can help insurers better prepare for and respond to severe weather events.

Government and community-level initiatives play a vital role in building resilience. This includes investing in resilient infrastructure, such as improved drainage systems, seawalls, and updated building codes that account for future climate risks. Land-use planning that discourages development in high-risk areas and promotes responsible land management practices is also critical. Public awareness campaigns to educate communities about weather risks and preparedness measures can empower individuals and businesses to take appropriate actions. The development of robust disaster preparedness and response plans, including effective evacuation procedures and post-disaster recovery support, is essential for minimizing the human and economic impact of destructive weather events. Collaboration between the public and private sectors is indispensable in fostering a comprehensive approach to risk reduction and adaptation in the face of increasing summer weather volatility. The long-term financial sustainability of the insurance market and the well-being of communities depend on embracing these proactive measures.

{kind=link}