The Inevitable Rise of Chatbots in Banking: A Strategic Imperative for Financial Institutions

The modern banking landscape is undergoing a radical transformation, driven by evolving customer expectations, technological advancements, and intense market competition. In this dynamic environment, banks that fail to embrace innovation risk becoming obsolete. Among the most potent forces reshaping customer interaction and operational efficiency within the financial sector is the chatbot. While some institutions have cautiously dipped their toes into this technology, the reality for virtually every bank, regardless of size or legacy, is that the adoption of sophisticated chatbots is not a matter of "if," but "when." This article will comprehensively explore the compelling reasons why banks need chatbots, outlining the strategic advantages and operational necessities that make them an indispensable component of future banking infrastructure.

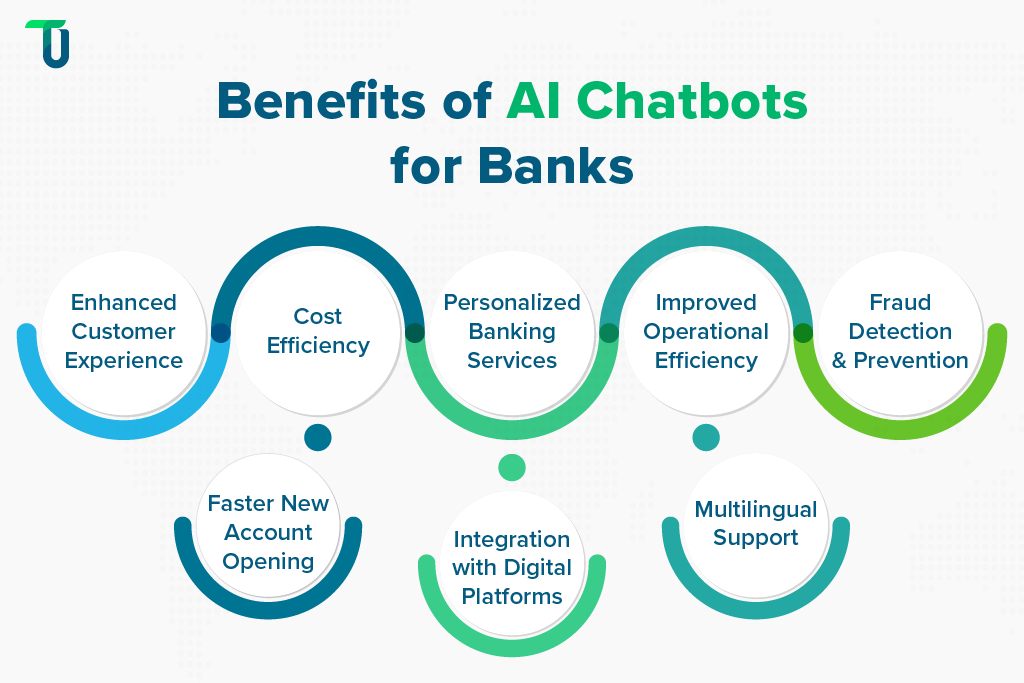

Customer expectations for instant, personalized, and accessible service are no longer a niche demand; they are the baseline for engagement across all industries. Consumers today are accustomed to interacting with intelligent virtual assistants in their daily lives, from ordering groceries to troubleshooting technical issues. This ubiquitous exposure has created a powerful expectation that financial institutions should offer similar levels of convenience and responsiveness. Traditional banking channels, such as phone calls and in-branch visits, often involve significant wait times, limited operating hours, and a fragmented customer experience. Chatbots, conversely, offer 24/7 availability, immediate responses to common queries, and the ability to handle multiple customer interactions simultaneously. This immediate gratification, coupled with the ability to access information and execute simple transactions at any time, directly addresses the core of modern consumer desires, significantly enhancing customer satisfaction and fostering loyalty.

Beyond mere convenience, chatbots represent a powerful tool for improving operational efficiency and reducing costs. A significant portion of a bank’s customer service workload comprises repetitive, low-value inquiries that can be easily automated. These include queries about account balances, transaction history, password resets, branch locations, and basic product information. By deploying chatbots to handle these routine tasks, banks can free up their human customer service agents to focus on more complex, high-value interactions that require human empathy, problem-solving skills, and in-depth financial advice. This reallocation of resources not only boosts the productivity of human staff but also leads to substantial cost savings by reducing the need for a large, round-the-clock human support team. Moreover, chatbots can be trained to collect initial information from customers before escalating to a human agent, streamlining the problem-solving process and further reducing resolution times.

The data-gathering and analytical capabilities of chatbots are another critical driver for their adoption. Every interaction a chatbot has with a customer generates valuable data. This data can be analyzed to gain deep insights into customer behavior, preferences, pain points, and emerging trends. By understanding which questions are asked most frequently, what products customers are inquiring about, and where customers encounter difficulties, banks can proactively identify areas for improvement in their products, services, and customer journeys. This data-driven approach enables banks to personalize offers, tailor marketing campaigns, and even predict potential customer churn. Furthermore, chatbots can assist in compliance-related tasks, such as gathering KYC (Know Your Customer) information or providing disclosures, contributing to a more robust and auditable record of customer interactions.

The competitive landscape in banking is intensifying, with both traditional institutions and fintech challengers vying for market share. Fintech companies, often unburdened by legacy systems, have been at the forefront of adopting innovative technologies, including AI-powered chatbots, to offer superior customer experiences and more agile services. To remain competitive, traditional banks must level the playing field by leveraging similar technologies. Chatbots offer a tangible way to differentiate a bank’s service offering, attract a younger, tech-savvy demographic, and retain existing customers who may be tempted by the seamless digital experiences offered by fintechs. The ability to provide instant, self-service options for common banking needs can be a significant competitive advantage in a crowded market.

Personalization is no longer a luxury but an expectation in the financial services sector. Customers want to feel understood and valued. Chatbots, when integrated with core banking systems and CRM platforms, can deliver hyper-personalized experiences. They can access individual customer data to provide tailored advice, recommend relevant products based on spending habits and financial goals, and even proactively alert customers to potential issues or opportunities. For instance, a chatbot could notify a customer about an upcoming bill payment, suggest a better savings plan based on their deposit history, or offer a pre-approved loan based on their creditworthiness. This level of personalized engagement fosters a deeper relationship between the bank and its customers, moving beyond transactional interactions to a more advisory role.

Scalability is a crucial consideration for any bank, especially during periods of high demand or rapid growth. Traditional customer service models struggle to scale effectively without a proportional increase in human resources, leading to service degradation and increased costs. Chatbots, however, are inherently scalable. They can handle an exponential increase in customer inquiries without a significant impact on performance or cost. This ability to scale seamlessly ensures that banks can maintain a high level of service delivery, even during peak times such as tax season, holiday periods, or following major product launches, without compromising on speed or accuracy.

Enhancing the digital onboarding process is another area where chatbots can prove invaluable. The initial onboarding of new customers can often be a complex and time-consuming process, with potential friction points that can lead to abandonment. Chatbots can guide new customers through the entire onboarding journey, collecting necessary information, answering questions, verifying documents, and explaining terms and conditions in an interactive and user-friendly manner. This not only speeds up the onboarding process but also significantly improves the customer experience, making a positive first impression and setting the stage for a long-term relationship. A smooth and efficient onboarding experience is critical for customer acquisition and retention.

The potential for fraud detection and prevention is a compelling, albeit often overlooked, benefit of sophisticated chatbots. By continuously monitoring customer interactions and transaction patterns, AI-powered chatbots can be trained to identify anomalies and suspicious activities that may indicate fraudulent behavior. They can ask clarifying questions during transactions or flag unusual inquiries for immediate human review. While not a replacement for dedicated fraud detection systems, chatbots can act as an additional layer of defense, providing early warnings and enabling quicker intervention, thereby protecting both the bank and its customers from financial losses.

Furthermore, chatbots can play a significant role in financial education and advisory services, democratizing access to financial guidance. Many individuals lack the financial literacy to make informed decisions about investments, savings, and debt management. Chatbots can be programmed to provide accessible, easy-to-understand information on a wide range of financial topics, tailored to the individual’s knowledge level and financial situation. They can offer guidance on budgeting, saving for retirement, understanding different investment options, and managing credit. This educational role not only empowers customers but also positions the bank as a trusted advisor, fostering long-term relationships and promoting financial well-being within its customer base.

The future of banking will undoubtedly be a hybrid model, where human interaction and AI-powered automation work in synergy. Chatbots will not replace human bankers entirely, but rather augment their capabilities, allowing them to focus on more strategic and empathetic tasks. The integration of chatbots is not merely a technological upgrade; it is a fundamental shift in how banks interact with their customers and manage their operations. Banks that fail to recognize this imperative and strategically implement advanced chatbot solutions will find themselves at a significant disadvantage in the evolving financial ecosystem. The journey towards a fully integrated, AI-driven customer experience, with chatbots at its forefront, is no longer a distant vision but an immediate necessity for survival and success in the modern banking era.

{kind=link}