Units for Debt Settlement: A Comprehensive Guide to Understanding and Optimizing Your Debt Resolution Strategy

The labyrinthine world of debt settlement often leaves consumers bewildered by the various options and pathways available for resolving their financial obligations. Understanding the "units" of debt settlement, which can be broadly categorized into organizational structures, service models, and financial mechanisms, is crucial for developing an effective strategy. This article provides a detailed exploration of these units, empowering individuals to make informed decisions and navigate the debt settlement landscape with greater clarity and confidence.

Organizational Structures in Debt Settlement:

The primary organizational units involved in debt settlement are debt settlement companies, credit counseling agencies, and bankruptcy attorneys. Each plays a distinct role and offers different approaches to debt resolution.

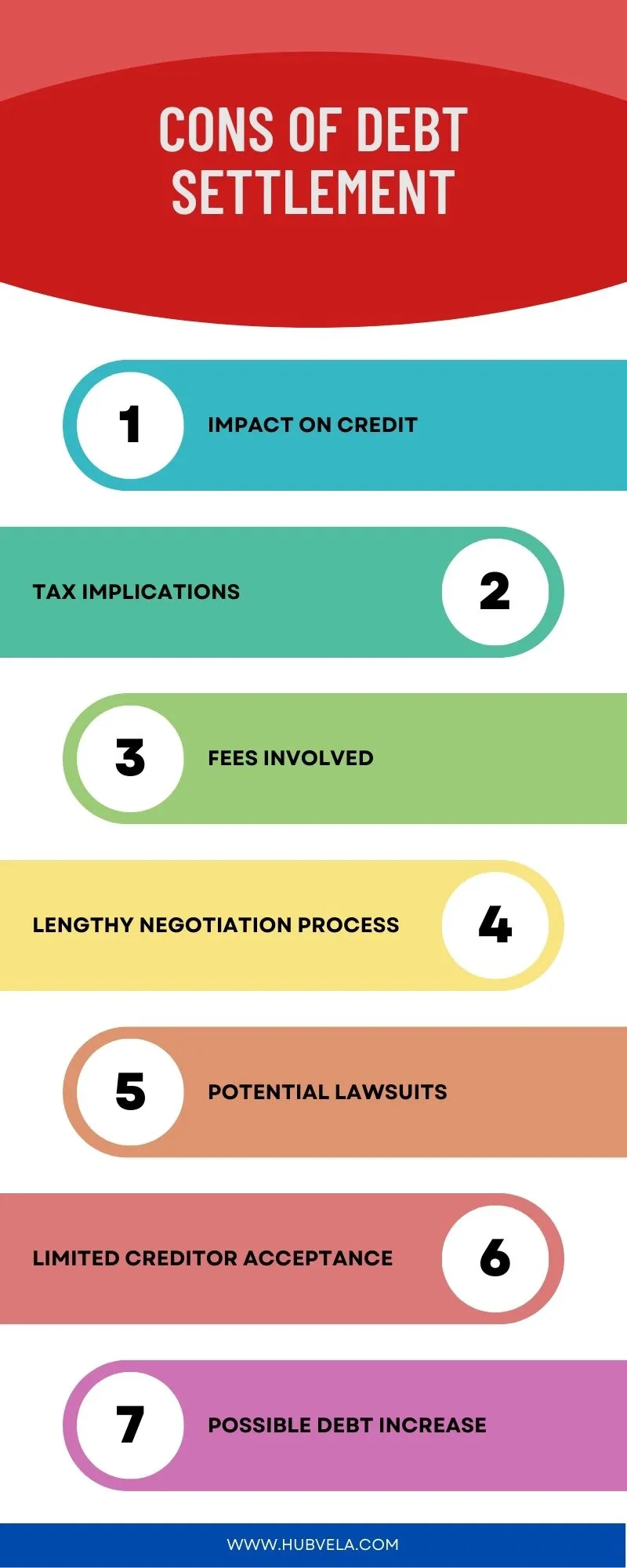

Debt Settlement Companies: These for-profit entities specialize in negotiating with creditors on behalf of consumers to reduce the principal balance owed. Their primary business model revolves around charging clients fees for their services, typically a percentage of the total debt enrolled in their program or a flat fee per settled debt. Debt settlement companies often operate by having clients deposit funds into a dedicated savings account. Once a sufficient amount is accumulated, the company uses these funds to make lump-sum settlement offers to creditors. The allure of debt settlement companies lies in their potential to significantly reduce the overall amount owed, offering a lifeline to individuals struggling with overwhelming unsecured debt. However, it’s imperative for consumers to thoroughly research any debt settlement company, scrutinizing their accreditation, reviews, and fee structures. Reputable companies will be transparent about their practices and the potential risks associated with debt settlement, such as the impact on credit scores and the possibility of lawsuits from creditors if negotiations fail. Understanding the specific services offered, the typical settlement percentages achieved, and the projected timeline for resolution is paramount.

Credit Counseling Agencies: These non-profit organizations offer a broader range of financial guidance, including budgeting, financial education, and debt management plans (DMPs). While some credit counseling agencies may offer debt settlement services, their core focus is often on managing debt through structured repayment plans rather than outright reduction. In a DMP, the agency negotiates with creditors to consolidate multiple debts into a single monthly payment, often with reduced interest rates and waived late fees. The consumer then makes one consolidated payment to the agency, which disburses it to the creditors. This approach can be more beneficial for individuals who can afford to repay their debts, albeit with some concessions from creditors. Credit counseling agencies are regulated and often accredited by organizations like the National Foundation for Credit Counseling (NFCC). Their emphasis on financial education and long-term financial well-being distinguishes them from purely profit-driven debt settlement companies. Consumers should verify the accreditation and the specific services offered by any credit counseling agency to ensure it aligns with their debt resolution goals.

Bankruptcy Attorneys: These legal professionals assist individuals in navigating the complex process of filing for bankruptcy. Bankruptcy, a legal proceeding, can offer a fresh start by discharging certain types of debt. The two most common consumer bankruptcy chapters are Chapter 7 (liquidation) and Chapter 13 (reorganization). A bankruptcy attorney will assess an individual’s financial situation, determine eligibility for different chapters, and represent them throughout the legal process. While bankruptcy can be an effective solution for severe debt situations, it has significant long-term consequences, including a substantial negative impact on credit scores for many years. The decision to file for bankruptcy should be made after careful consideration and consultation with a qualified attorney. Understanding the legal implications, the types of debts that can and cannot be discharged, and the specific procedures involved is critical.

Service Models in Debt Settlement:

Beyond organizational structures, debt settlement can be approached through various service models, each with its own operational framework and client interaction.

Do-It-Yourself (DIY) Debt Settlement: This model involves individuals directly negotiating with their creditors without the assistance of a third-party company. This approach requires significant time, effort, and negotiation skills. The primary advantage is the avoidance of third-party fees. However, it can be emotionally taxing and may not be suitable for individuals who are unfamiliar with negotiation tactics or who are overwhelmed by the prospect of interacting with creditors. Success in DIY debt settlement hinges on a thorough understanding of creditor policies, legal rights, and effective communication strategies. Researching best practices for debt negotiation, understanding consumer protection laws, and preparing a compelling case for a reduced settlement amount are essential components of this model.

Third-Party Negotiation Services: This encompasses the services provided by debt settlement companies and some credit counseling agencies, where a professional intermediary negotiates with creditors on the consumer’s behalf. The core principle here is leveraging the expertise and established relationships of these organizations to achieve more favorable settlement terms than an individual might achieve on their own. These services typically involve a fee structure, which can be a percentage of the enrolled debt or a per-settlement fee. The benefits include relieving the consumer of the stressful negotiation process and potentially achieving higher settlement rates due to the company’s experience and volume of business. It’s crucial to evaluate the fee structure, the company’s track record, and the transparency of their processes before engaging their services. Understanding how they handle communication with creditors, the expected timelines, and the potential impact on credit scores is vital for making an informed decision.

Managed Debt Repayment Plans: This model, often employed by credit counseling agencies through Debt Management Plans (DMPs), focuses on structured repayment rather than aggressive settlement. The agency acts as a facilitator, consolidating payments and negotiating interest rate reductions. The consumer makes a single, often reduced, monthly payment to the agency, which then distributes the funds to creditors. This model is ideal for individuals who can afford to repay their debts but are struggling with high interest rates and multiple payment due dates. The key benefit is the simplification of debt management and the potential for significant interest savings over time. It’s important to understand the fees associated with the DMP, the duration of the plan, and the specific terms negotiated with creditors to ensure it aligns with the individual’s financial capacity and long-term goals.

Financial Mechanisms in Debt Settlement:

The financial underpinnings of debt settlement involve various mechanisms for managing funds and executing transactions.

Dedicated Savings Accounts: Many debt settlement programs require clients to deposit funds into a dedicated savings account. This account is typically controlled by the debt settlement company, which then uses the accumulated funds to make settlement offers to creditors. This mechanism serves to create a pool of capital that can be utilized for lump-sum payments, which are often more effective in securing reduced settlement amounts. The transparency of this account, including statements and accessibility for the consumer, is a critical factor in selecting a reputable debt settlement provider. Understanding who holds the title to the account and how the funds are managed is essential to prevent potential misuse.

Lump-Sum Settlement Offers: The cornerstone of many debt settlement strategies is the lump-sum settlement offer. This involves paying creditors a reduced amount of the total debt owed in a single, immediate payment. The rationale behind this approach is that creditors are often willing to accept a lesser amount to avoid the protracted and uncertain process of collecting the full debt, especially if the debt is significantly past due. Successful lump-sum settlements require sufficient capital to be accumulated in the dedicated savings account, along with effective negotiation by the debt settlement company. The percentage of the debt that can be settled typically varies depending on factors such as the age of the debt, the creditor’s policies, and the overall economic climate.

Debt Consolidation Loans: While not strictly a debt settlement mechanism that reduces the principal owed, debt consolidation loans can be a component of a broader debt resolution strategy. These loans allow individuals to combine multiple existing debts into a single new loan, often with a lower interest rate. This can simplify repayment by consolidating multiple payments into one manageable monthly payment. However, if the new loan’s interest rate is not significantly lower, or if the repayment term is extended, the overall cost of debt repayment may not be reduced. Debt consolidation loans can be obtained from banks, credit unions, or online lenders. It’s crucial to carefully compare interest rates, fees, and repayment terms before taking out a consolidation loan to ensure it truly offers a financial advantage.

Debt Buyouts and Portfolio Sales: In some instances, creditors may sell portfolios of delinquent debt to third-party debt buyers at a steep discount. These debt buyers then attempt to collect on the debt, often for less than the original amount owed. Consumers may have the opportunity to negotiate with these debt buyers for a settlement. This can sometimes result in lower settlement amounts than negotiating directly with the original creditor, but it can also introduce a new party into the collection process. Understanding who currently owns the debt and their willingness to negotiate is a key aspect of this financial mechanism.

Key Considerations and SEO Optimization:

When discussing units for debt settlement, employing specific keywords and phrases relevant to consumer finance and debt resolution is crucial for SEO. This includes terms like "debt settlement companies," "credit counseling," "debt management plans," "bankruptcy," "debt negotiation," "reduce debt," "lower interest rates," "financial hardship," "debt relief," and "credit score impact." Providing actionable advice, clear definitions, and comprehensive explanations of each unit will enhance the article’s value and improve its ranking in search engine results. The article’s structure, with clear headings and subheadings, also aids in readability and SEO. Utilizing internal and external links to relevant resources can further boost its authority. The objective is to create a definitive resource that answers the most common questions consumers have about debt settlement units, thereby driving organic traffic and establishing the article as a trusted source of information. The detailed exploration of each unit, from organizational structures to financial mechanisms, ensures that a broad spectrum of user queries related to debt settlement is addressed.

{kind=link}